Over $1 billion in pub assets changed hands in New South Wales and Queensland in FY19, according to a report analysing every transaction for the year.

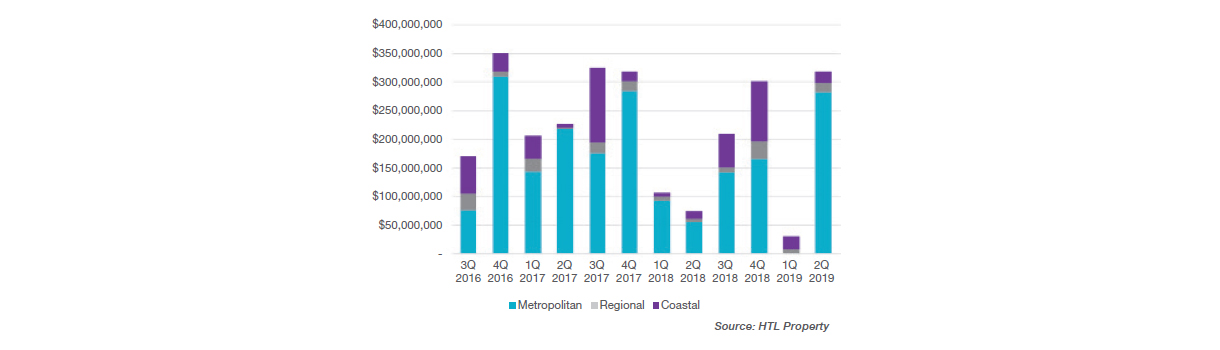

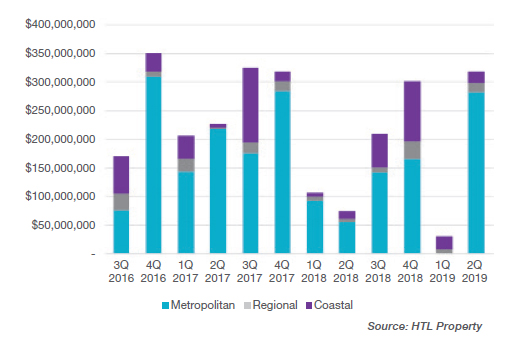

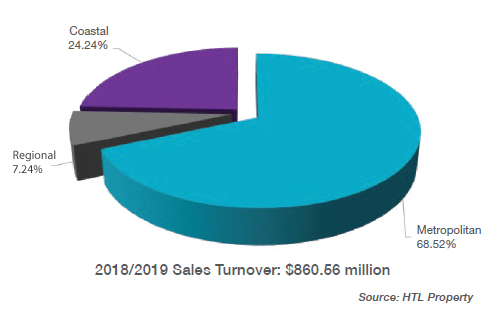

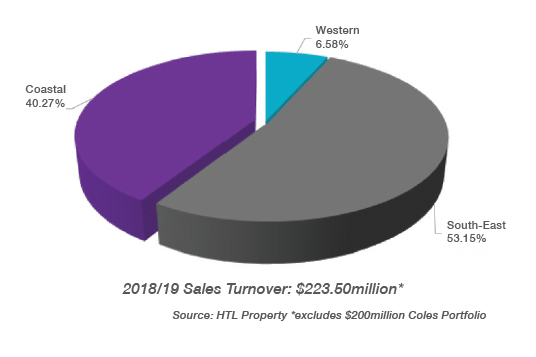

NSW rebounded in the final quarter to record $860m in industry sales for the year, across 66 transactions, while Queensland recorded $223m across 22 transactions, discounting the $200m portfolio sale of Coles’ pubs, which was excluded from the analysis.

The study by HTL Property chronicles the 2018/19 financial year as the company celebrates its first year in business, citing 44 sales on the books at gross value of $450m.

The detailed report notes three main events affecting the market during the period, most notably seen in the historically low 1Q period in NSW transactions.

March’s Federal Election was seen as one major inhibitor on market activity, with economic policies threatening to alter the investment and real estate landscapes. The return to government of the Coalition suggests economic reforms will be minimal.

The Financial Services Royal Commission, which began at the end of 2017, was tasked with investigating widespread misconduct within the banking, superannuation and financial services industries, after years of public and consumer pressure to do so.

The investigation led to banks tightening lending criteria, dampening investor sentiment and activity.

The Commission submitted its final report in February 2019, and accessibility to credit is said to have already dramatically improved since.

And ending a three-year period without change, in July the Reserve Bank cut the official interest rate by 0.25 per cent to a new record low of 1.0 per cent. The RBA had been under mounting pressure to further stimulate the economy, in light of consumers reducing spending and unemployment beginning to rise.

“There have already been signs of improved investor sentiment immediately following the rate cut, with buyers becoming more active and revising previous views on the pricing of hotel assets,” notes the report.

NSW Regional and Coastal sales were seen as big performers, assisted by buoyant gaming entitlement prices, now enjoying characteristics previously only found in the Metropolitan market.

“With cap rate compression and deals being done on an opportunity basis, purchasers are happy to share in some of the upside with vendors, via tighter yield events.”

In March 2018 NSW Parliament passed amendments to the Gaming Machines Act 2001.

This included permissible leasing of entitlements for venues with 10 PMEs or less, which while agreements have been limited and supply has largely outweighed demand, the company says was a “game-changer” for some parties.

Leases have taken place for $14-18k p/a per entitlement, equating to an 8-11 per cent return on current values.

The changes to Band classifications saw Band 1 entitlement prices peak at around $200k each, as savvy operators rushed to fill newly permissible thresholds. As a number of regional operators listed toward the end of 2018 prices softened to $160–165k per, but have since stabilised around $175-180k, consistent with the three- to four-year average.

Queensland gaming machine authority prices remained relatively stable. Only three tenders took place through the year, most recently in April, where an abnormally large quantity of 88 machines were surrendered and sold in the south-east, averaging $169,597.

“With Queensland Liquor and Gaming Legislation being arguably the tightest in the country, the future prospects for the industry are attractive for both its stability and growth prospects.”

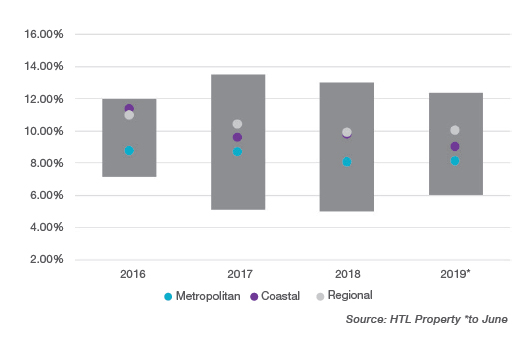

Conditions have combined to sustain yield contraction; HTL projects the NSW Coastal market will hold at its current range of 9-11 per cent, and Regional will hold at 11-13 per cent.

The company forecasts the Sydney Metro market to sharpen up to 50 basis points from current levels, believing 7.50 per cent is achievable for prime assets, up to 8.50 per cent for suburban assets with strong underlying fundamentals.

North of the border, the Queensland market is operating at 9.25-10.50 per cent for the south-east, and 10.50-12.50 per cent representative of the broadening geographical Regional asset spread.

Looking to the future, HTL’s report notes well-funded groups are forming a formidable force in acquisitions, but double-digit cash-on-cash returns are “still well and truly achievable” even in sharp Metro purchases, on the LVRs available.

“This cannot be duplicated in most other asset classes,” says national director Dan Dragicevich.

And with government in NSW and Canberra locked in for the next few years, HTL notes a sharp increase in buyer enquiry.

“We expect this to continue throughout the next 12 months,” furthers Dragicevich.

“The lending environment is liquid for those well capitalised operators with proven operational experience, and clearly the rates at which capital can be borrowed is at an historical low.

“The resultant spread between borrowing costs, and what might be perceived as currently sharp cap rates, is still compelling, and is at its core what continues to drive demand and transactional activity.”