In the past two financial years insolvencies in Australia have climbed dramatically compared to pre-pandemic levels, disproportionately affecting small and medium businesses such as hospitality.

The post-pandemic business in Australia is battling change across multiple areas, seeing increases in interest rates, labour market challenges, global supply chain pressures and shifting consumer behaviour.

The monthly Business Risk Index (BRI) by CreditorWatch provides a real-time view of the financial health of Australian businesses, tracking the likes of insolvencies, defaults, failure rates and broader business conditions. Data is provided nationally, by state, region and industry and can highlight emerging trends before they appear in official economic statistics.

A report provided by CreditorWatch has outlined areas of concern, including insolvency and business failure trends and industry performance.

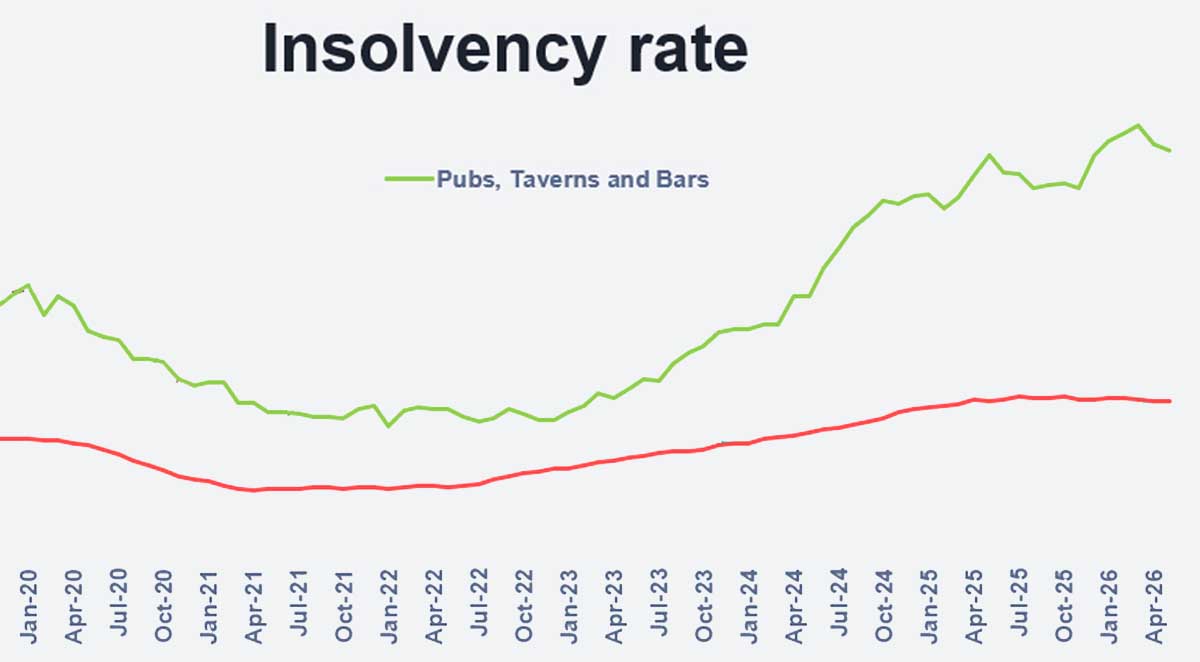

The sector of ‘Pubs, Taverns and Bars’ saw a peak in insolvencies late 2019 (above), then a high late 2022 likely a result of interest rate and supply stresses after the pandemic.

However, another high took place mid-2025, as insolvencies more than doubled (35,774 in FY24 to 84,529 in FY25) – against the overall business average of a roughly 20 per cent increase.

Insolvencies typically lag underlying pressures by 12-18 months.

There were five interest rate increases across 2023, and while cashflow may be affected quite quickly, formal administrations take time to flow through.

Also, FY25 saw a surge in the ATO issuing garnishees and Director Penalty Notices (DPNs), as it sought to claw back debt that had blown out during COVID, during which it took a ‘hands off’ approach to collection. Once this process was executed and the tax office’s debt reduced, insolvencies did decrease again.

Despite the challenges of the economic conditions, most businesses that fall into insolvency actually do so because they treat financial strategy as an afterthought.

There are typically clear warning signs that many business owners overlook or ignore, until they become existential. Trading while insolvent invites heavy penalties, including directors facing personal liability.

An early warning sign is initial cashflow irregularities and an increasing reliance on credit. As financial strain continues there may be difficulty meeting tax obligations and payment terms.

In the final months prior to the end the business may struggle to meet payroll or other essential obligations and see increasing pressure from creditors.

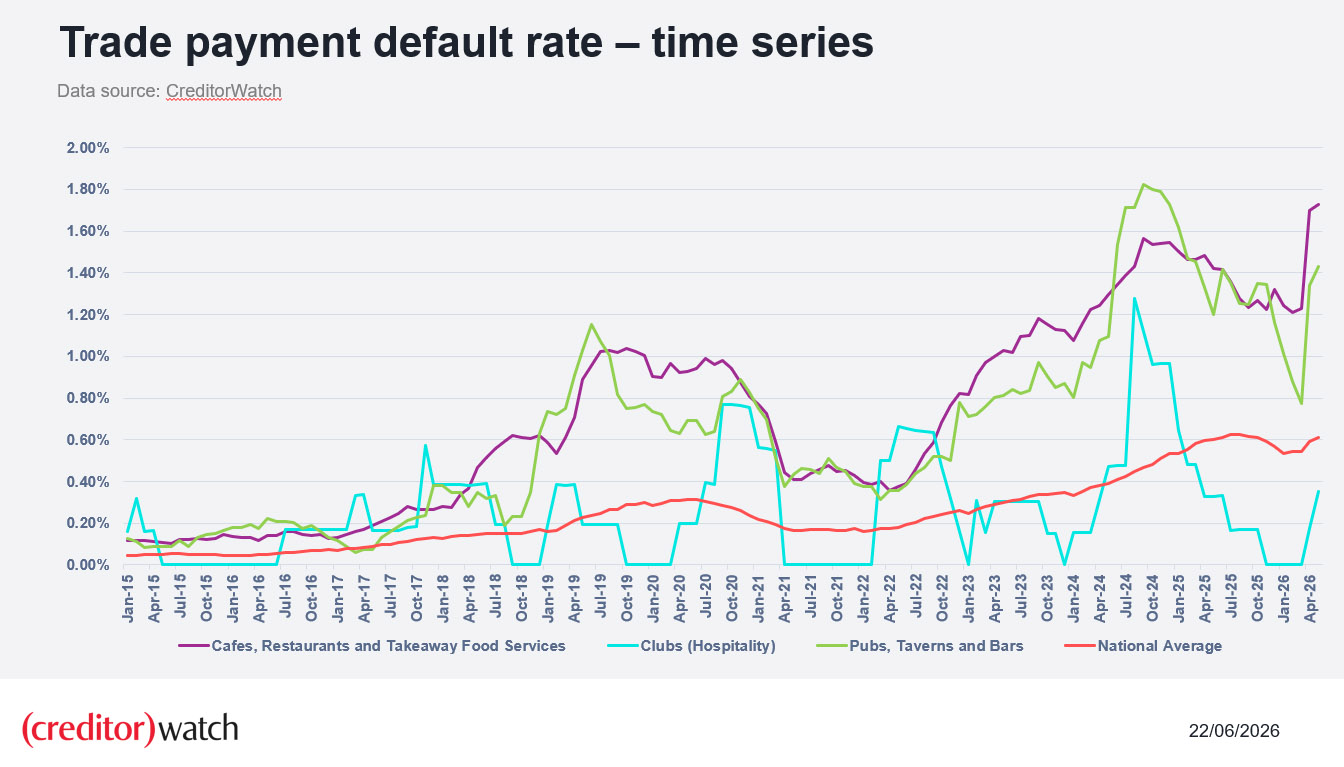

The CreditorWatch data shows how payment defaults peaked mid-2024, in pubs and clubs, which is indicative of the effects on cashflow by high interest rates, and precedes the insolvencies seen in 2025. Data also shows a high point in payments in arrears in early 2026, amid the rising cost of living.

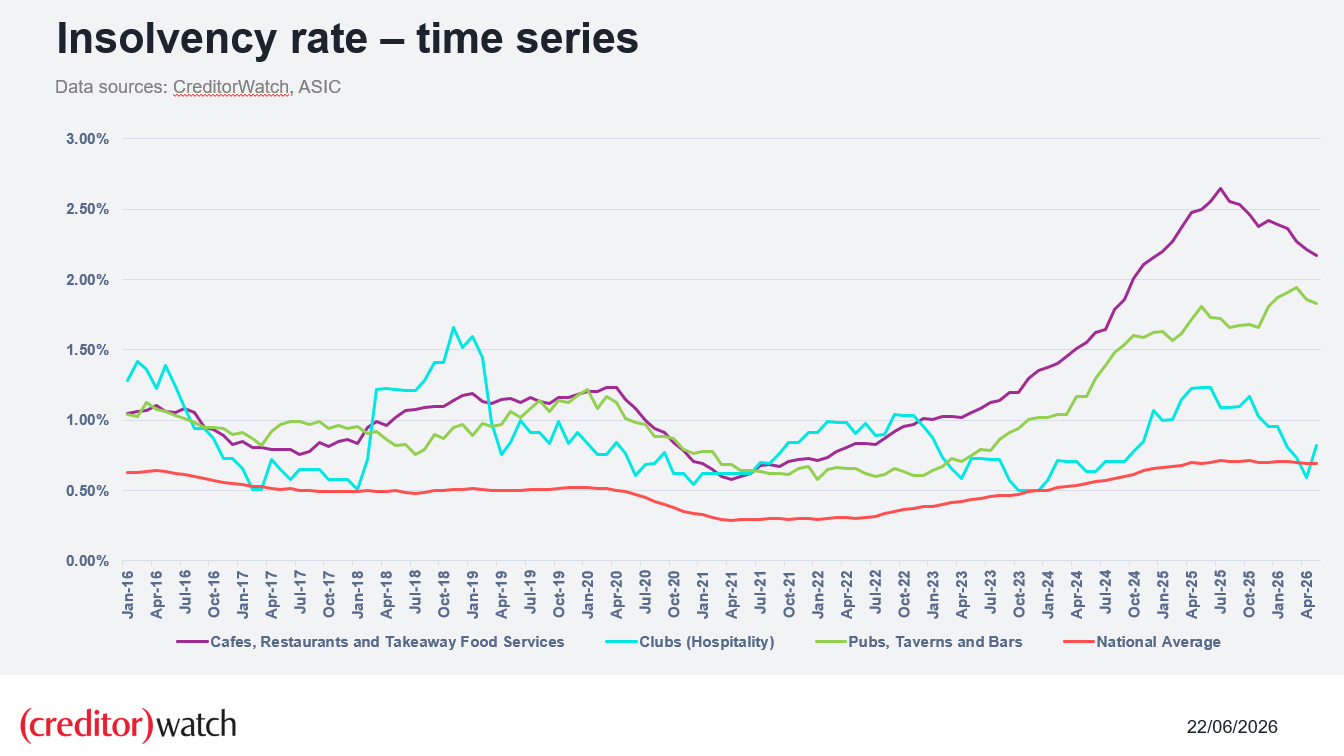

While insolvency rates for the pubs sector have continued to trend upwards, these are driven more by the closures of small bars than of pubs, although CreditorWatch says all small businesses are more vulnerable to economic downturns, typically having smaller cash buffers and operating on tighter margins.

“Small bars have also experienced cost pressures from higher rents, energy prices, wages, insurance and inputs such as F&B,” notes CreditorWatch chief economist Ivan Colhoun.

“On top of that they have experienced reduced demand from consumers due to cost-of-living pressures.”

There are critical blind spots classically affecting many small businesses, often led by inadequate cashflow management; ASIC data shows two thirds of small businesses entering insolvency had no formal system for forecasting cashflow. Further to this, many have inadequate ability to forecast their financials.

Also, there is reactive, short-term thinking, which may address symptoms but not the underlying problems, and frequently leads to temporary cost-cutting, which can hinder operations and damage the customer experience. Cost-cutting won’t save the business if the problem is really pricing, a lack of recurring revenue or simply cashflow management.

SMEs can build on their financial resilience by producing or acquiring a suitable framework for this, with ongoing (13-week) forecasts, building an emergency cash reserve and establishing early warning systems to flag issues.

“We expect insolvencies to trend up again as cost pressures remain high and cost-of-living pressures affect consumers,” says Colhoun.

“Once costs rise for things like rents, wages, insurance, and food and beverage they don’t come down again – they’re permanently baked in.”