ALE’s results for FY18 herald continued strength in the Australian pub sector, showing strong valuations, record low debt and market-leading returns for investors.

Listed entity ALE (ASX: LEP) is the biggest landlord to Australia’s biggest publican, the majority Woolworths-owned Australian Leisure & Hospitality (ALH). All of ALE’s 86 properties are ALH-tenanted pubs, with 83 of these on triple-net leases.

ALH operate over 330 pubs, many of them leaseholds, collectively turning over $4.3bn in FY18, with EBITDA exceeding $800 million (around 19 per cent).

ALE’s 95-Ha of land is predominantly in capital cities, and the year saw valuations up five per cent ($54.7m) to more than $1.1bn, aided by ongoing capex by ALH, which still enjoys below-market rents on the freeholds.

ALH rents are fixed to CPI, but a major review this November will see most go up by as much as ten per cent, as allowed for in the lease. The next major review in 2028 will not be capped and may see many change significantly to align with market value.

WALE (Weighted Average Lease Expiry) across the ALE portfolio is around ten years.

At the same time, record low interest rates and ongoing debt reduction see ALE’s gearing fall to an all-time low of 41 per cent, with total net debt below $500 million.

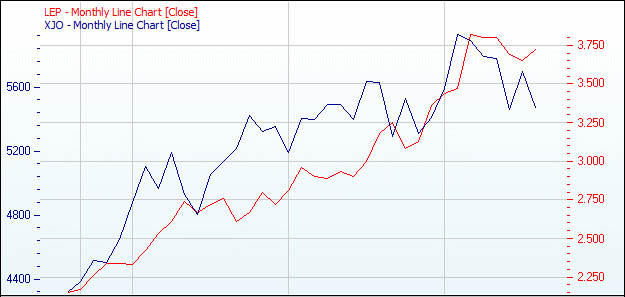

The perfect storm sees an investment market-topping return to security-holders of 24.5 per cent, still in the company’s practice of 100 per cent tax deferred, although this will begin to end in FY19.