Live entertainment is a regular feature in many pubs and clubs, with venues engaging musicians, DJs, comedians, MCs and other performers throughout the year.

While many of these engagements are made with contractors who provide an ABN, that does not necessarily mean there is no obligation to pay superannuation.

Under the new Superannuation Guarantee (SG) legislation, when an individual is paid mainly for their labour, for SG purposes they are to be treated as an employee.

This means venues must pay SG (currently twelve per cent of wages) to the individual’s super fund at the same time as the wages (“Payday Super”). Payday Super remains a draft ruling until the end of the month.

Between 1 July 2022 and 1 July 2026 there was a $450 earnings threshold – this threshold no longer exists, meaning even lower-value and occasional bookings may require SG.

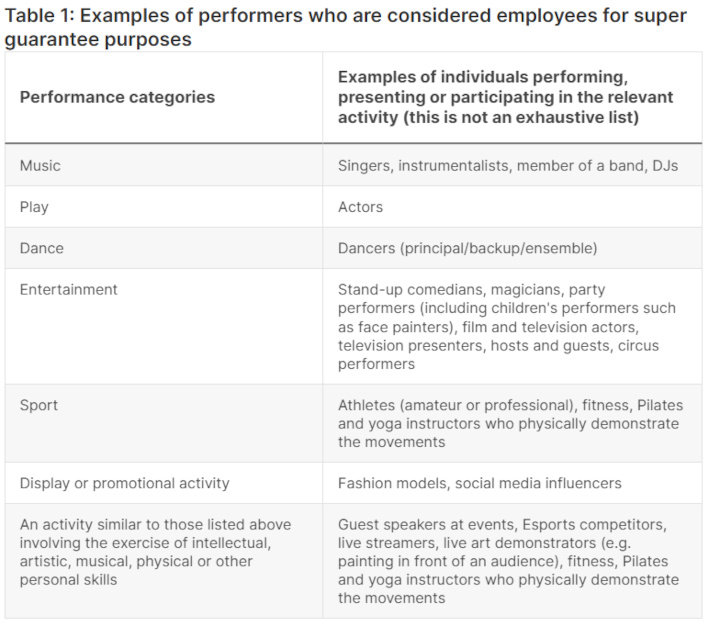

The rules contain specific provisions covering performers, sportspeople and individuals involved in film, television, radio and related entertainment activities.

For licensed venues, this means that the existence of an ABN or contractor agreement is not, on its own, enough to determine whether super is payable.

The legislation generally applies where an individual is engaged to perform or participate in an entertainment activity.

Depending on the nature of the engagement, some individuals providing services directly connected with those performances (such as lighting or sound) may also be covered.

The position may differ where the venue contracts with an entertainment agency or production company instead of engaging an individual directly. In those cases, responsibility for super will depend on the contractual arrangements and the entity supplying the services.

Failure to meet SG obligations can be costly. Where super should have been paid but was not, employers may become liable for the Superannuation Guarantee Charge, together with interest and administrative penalties.

With live entertainment continuing to play an important role in attracting patrons, contractor arrangements involving performers should be reviewed periodically to ensure SG obligations are being met.

This is particularly relevant for venues that regularly engage individual entertainers rather than booking through an agency or incorporated business.

A contractor’s ABN is only one part of the picture. For superannuation purposes, the legislation looks at the substance of the arrangement, and in many cases, performers engaged directly by a venue may still be entitled to super contributions.

The fallout due to these new regulations has been immediately apparent.

For example, the organisers of the Newcastle Hunter Jazz Festival recently announced the cancellation of its decades-old event, blaming the administrative burden of complying with superannuation obligations.

“For over 300 musicians at the jazz festival, this is a logistical nightmare for the NHJC, as we are volunteers, and have no payroll software to manage this process,” the announcement said.

Responses on social media were also immediate, pointing out that no arts organisations or musicians were invited to collaborate in creating the legislation.

“This legislation is not fit for purpose and fails spectacularly to understand the sector and to address the actual nature of collective collaboration in music across the board,” said one post.

“It harms small regional orchestras it harms big bands. It is already harming jazz festivals and small venues. The ATO itself cannot understand the legislation and is giving incorrect advice left right and centre. The conflicting advice is staggering,” it continued.

Other reactions included some describing the changes as an increased compliance burden that may encourage venues to engage incorporated entities instead of sole traders, while others say the additional costs and administration have already resulted in cancelled gigs.

The public may respond to the draft ruling until 31 July.

This article is general in nature. Please refer to ATO and legislation sources for current law and dates and to financial experts for advice.